Refinancing isn't just about chasing a lower interest rate. It's about making your mortgage work harder for you. Whether you're looking to cut repayments, unlock equity, or gain features that give you more financial control, smart refinancing can transform your financial position.

Australia's mortgage landscape has changed dramatically in recent years. Interest rates have fluctuated, property values have shifted, and lenders have adjusted their policies. What suited you five years ago might now be limiting your options. This guide shows you exactly when and how to refinance strategically.

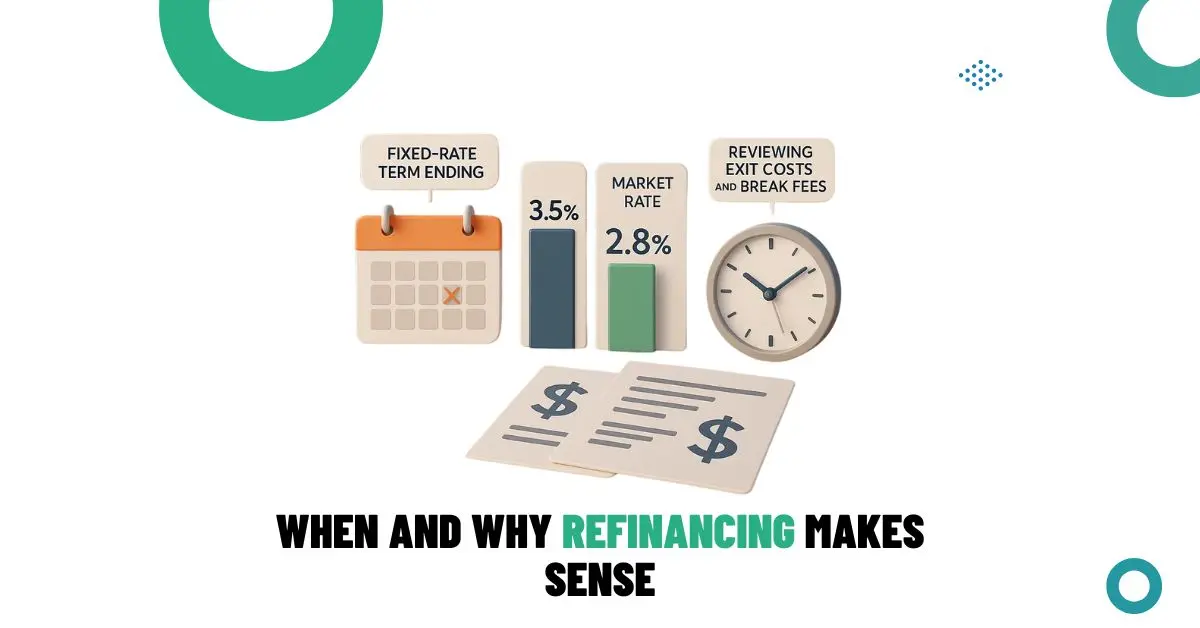

When and Why Refinancing Makes Sense

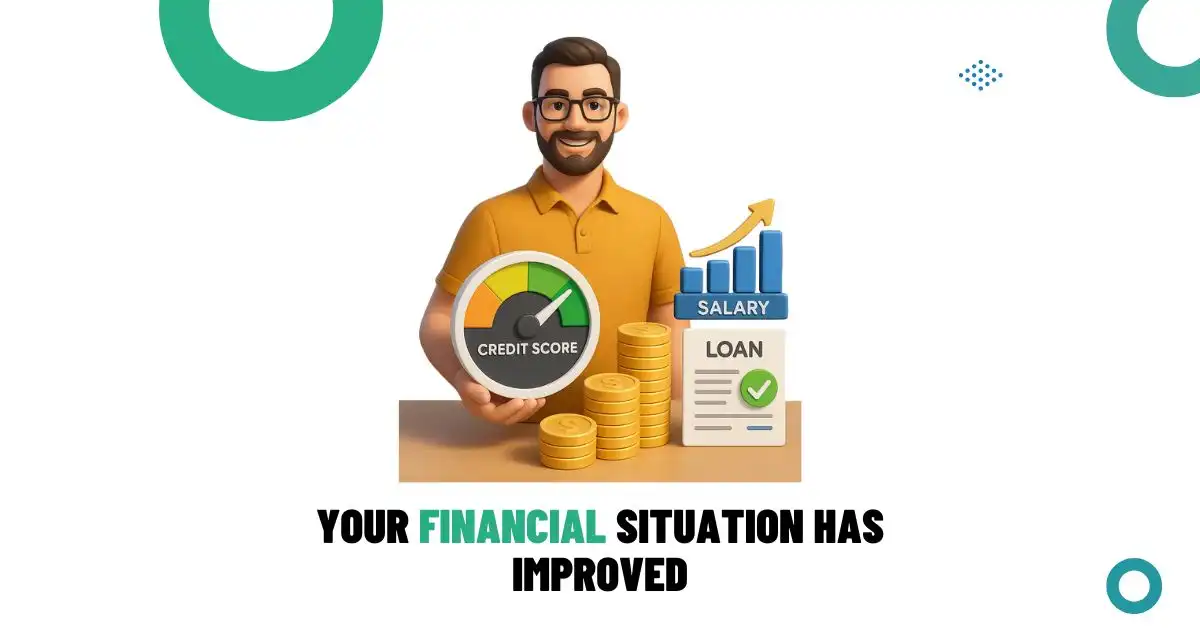

Your Financial Situation Has Improved

Timing a refinance correctly can save you tens of thousands over your loan's life. Doing it too often eats into savings through fees, but ignoring the right moment costs even more. Understanding when to make your move is crucial.

Your Fixed Rate Term Is Ending

When your fixed period expires, lenders automatically roll you fonto their standard variable rate, which is rarely competitive. This is prime time to review all your options.

Start comparing what other lenders offer three months before your fixed term ends. Look at both rates and features like offset accounts or unlimited extra repayments. Borrowers who proactively shop around when coming off fixed rates typically secure rates 0.3-0.8% lower than their lender's revert rate. On a $500,000 loan, that's $125-$333 saved monthly.

Check Your Current Rate Against Market Rates

Most borrowers don't realize they're paying above-market rates until they check. Banks rarely volunteer to lower your rate without being asked.

Visit comparison sites or speak with a broker who has access to wholesale rates across multiple lenders. Compare your current rate against new customer rates from at least five different lenders. The ACCC found that borrowers on legacy rates pay on average 0.62% more than new customers at the same bank for identical products.

Review Exit Costs and Break Fees

Breaking a fixed loan early can trigger substantial fees. But if rates have dropped significantly, even with break costs, you might save money by refinancing now.

Request a payout figure from your current lender. This includes your remaining balance plus any break costs. Compare this against potential savings over the remaining term. If you're more than 18 months from your fixed term ending and rates have dropped by 1% or more, break costs are often worth paying.

Time Your Application Strategically

Applying too early means dealing with expired valuations or pre-approvals. Too late, and you're stuck paying higher rates for months while processing.

Begin the refinance process 6-8 weeks before your fixed term ends. This gives enough time for approvals, valuations, and settlement without rushing. Brokers can lock in rates for up to 90 days with most lenders, protecting you if rates rise during processing.

Your Financial Situation Has Improved

Better income, higher credit score, or lower debt means you qualify for premium rates and better loan features you couldn't access before. Lenders assess your borrowing power at application. If your situation has strengthened since your original loan, you're now a lower-risk borrower.

A credit score improvement from good (600-699) to very good (700-799) can reduce your interest rate by 0.2-0.5%, saving $80-$210 monthly on a $500,000 loan.

Improved Credit Score Opens Better Deals

Lenders reserve their best rates for borrowers with excellent credit (750+). If you've been rebuilding credit, you might now qualify for premium pricing.

Get your free credit report from Equifax, Experian, or Illion. Scores above 700 qualify for preferred rates with most major lenders. Research shows borrowers with excellent credit scores (800+) receive rates up to 0.8% lower than those with average scores for identical loans.

Higher Income Increases Borrowing Options

Higher income not only increases how much you can borrow but also gives you access to lenders who have minimum income requirements for their best products.

If your income has increased by 20% or more since your original loan, you can likely access premium lender tiers or consolidate other debts into your mortgage at a lower rate.

Lower Debt-to-Income Ratio Strengthens Your Position

Lenders assess how much of your income goes toward debt repayments. Lower ratios signal stronger financial management and unlock better rates.

Paying down credit cards, car loans, or personal loans before refinancing improves your debt-to-income ratio and borrowing power. Lenders prefer ratios below 30%. Reducing yours from 40% to 25% can improve your rate by 0.3-0.5%.

You Want to Consolidate Debt

Combining high-interest debts (credit cards at 20%, personal loans at 12%) into your mortgage at 6-7% saves significant money and simplifies repayments. Refinancing lets you roll multiple debts into one loan with lower interest and longer terms, reducing monthly outgoings immediately.

Borrowers who consolidate $30,000 in credit card debt into their mortgage typically save approximately $350-$450 monthly in interest charges.

Calculate Total Interest Savings First

Don't just look at lower monthly payments. Extending debt over 30 years can cost more in total interest despite lower rates.

Add up current monthly debt repayments and total interest over remaining terms. Compare against the same debt consolidated into your mortgage at the new rate. Plan to maintain current repayment levels even after consolidating. This pays off the consolidated debt faster and maximizes savings.

Avoid Reaccumulating Debt After Consolidation

The biggest risk of debt consolidation is clearing credit cards, then running them up again. You've now doubled your debt problem.

Close or significantly reduce limits on credit cards after consolidating. Use debit cards or low-limit credit cards for emergencies only. Studies show 30% of borrowers who consolidate debt reaccumulate similar debt levels within 3 years.

Structure the Loan to Pay Debt Off Faster

Consolidating into your 30-year mortgage without a plan means paying off credit card debt over decades.

Use a split loan structure: consolidate debt into one portion with a 5-year term and aggressive repayments, keeping your existing mortgage separate. This approach combines lower interest rates with forced discipline, ensuring debt is cleared quickly while still reducing monthly cashflow pressure.

Strategic Refinancing Methods That Work

Refinancing is part numbers, part planning. The smartest borrowers don't just switch for a lower rate. They use refinancing to restructure their entire financial position.

Compare Rates But Look Beyond the Numbers

The lowest advertised rate isn't always the best deal. Some lenders offer teaser rates that jump after 12 months, or strip out essential features that cost you more long-term.

Look at comparison rates (which include most fees), loan features like offset accounts, and whether rates are discounted or standard. A rate 0.1% higher with full features often beats a stripped-back product. ASIC found 45% of borrowers who chose the "lowest rate" product ended up paying more over 5 years.

Use a Broker to Access Wholesale Rates

Brokers compare 30+ lenders at once and often access better rates than you'd get directly, especially from smaller lenders who don't advertise publicly. They see wholesale rate cards and know which lenders are aggressively competing right now.

Broker-sourced loans average 0.15-0.25% better rates than direct applications to the same lender.

Check Comparison Rates, Not Just Interest Rates

Interest rates exclude most fees. Comparison rates include application fees, ongoing fees, and some other costs, giving you the true cost of borrowing.

By law, lenders must display comparison rates. Use these to compare apples-to-apples across different products. Comparison rates assume you'll keep the loan for 25 years. If you're refinancing again in 2-3 years, upfront fees matter more.

Avoid Honeymoon Rates Without a Strategy

A 5.5% rate for 12 months that reverts to 7.2% looks great initially but costs you more in years 2-5 than a consistent 6.3% rate.

Honeymoon rates work if you're planning to refinance again in 12-18 months anyway. If you're not planning another refinance soon, choose a standard rate. Stability beats short-term savings that evaporate quickly.

Unlock Equity and Put It to Work

As your property increases in value and you pay down your loan, you build equity. Refinancing can access this equity without selling your home. Refinance for a higher loan amount based on your property's current value. The difference between your old loan and new loan is your accessible equity.

Australian property values have grown an average of 6-8% annually over the past decade, meaning most borrowers have significant untapped equity.

Use Equity for Renovations That Add Value

Borrowing against equity at 6% to fund renovations that increase your property value by 15-20% is one of the smartest uses of leverage.

Get quotes from builders first, then refinance for the exact amount needed plus a 10% buffer. Use a separate split loan for the renovation portion to track costs. A $60,000 kitchen and bathroom renovation typically adds $80,000-$100,000 to a home's value.

Invest Equity Into Property or Business

Using home equity to buy an investment property or fund business growth is how many Australians build substantial wealth over time.

Keep your principal home loan separate from investment borrowing. This protects your home if investments underperform and maintains tax deductions on investment debt. Only borrow against equity if you have stable income and can service both loans comfortably.

Balance Equity Use With Loan Serviceability

Accessing too much equity increases your loan-to-value ratio (LVR) and monthly repayments. This can limit future borrowing capacity or create repayment stress.

Keep your LVR below 80% when accessing equity. This avoids Lenders Mortgage Insurance and maintains your borrowing buffer. Only access equity if your total loan repayments stay below 30% of your gross household income.

Adjust Your Loan Structure for Flexibility

Your life evolves. Your loan should too. The right structure gives you options: make extra payments when you can, access funds when you need them, or balance security with opportunity.

Split loans, offset accounts, and variable-fixed combinations let you customize your mortgage to match your financial goals. According to ABS data, 62% of refinancing borrowers change their loan structure, not just their rate.

Split Between Fixed and Variable Rates

Fixed rates provide repayment certainty and protection from rate rises. Variable rates let you make unlimited extra repayments and potentially benefit from rate drops.

Many borrowers split 50/50 or 60/40 (variable/fixed). This balances predictability with flexibility. A borrower with a $600,000 loan might fix $300,000 at 5.8% for 3 years (certainty) and keep $300,000 variable at 6.1% (flexibility for extra repayments).

Add an Offset Account for Interest Savings

Every dollar in your offset reduces the balance you pay interest on. It works like making extra repayments but keeps your money accessible.

With $30,000 in a 100% offset account linked to a $500,000 loan at 6%, you save $1,800 annually in interest while maintaining full access to that $30,000. Direct all income into your offset account and pay bills from there. This maximizes the time your money offsets your loan balance.

Shorten or Extend Loan Terms Strategically

Shorter terms mean higher repayments but massive interest savings. Longer terms reduce monthly pressure but cost more over time.

If cashflow is tight, extending from 20 to 25 years reduces monthly repayments significantly. If you've had income growth, shortening from 30 to 20 years saves tens of thousands. Shortening a $500,000 loan from 30 to 25 years at 6% saves approximately $95,000 in total interest, despite monthly repayments increasing by $330.

Take Control of Your Home Loan Today

Refinancing isn't about chasing trends or reacting to advertisements. It's about creating financial flexibility that grows with you. By reassessing your loan every 2-3 years, you ensure it still fits your goals, income, and lifestyle.

Whether you're upgrading your home, funding renovations, consolidating debt, or simply looking to reduce repayments, smart refinancing puts you back in control. Start by checking your current rate against the market, calculating potential savings, and speaking with a mortgage broker who can show you options you didn't know existed.

When done strategically, refinancing isn't just a money-saving move. It's a step toward financial independence and making your mortgage work for you.

Frequently Asked Questions About Refinancing Your Home Loan in Australia

Q1. When is the best time to refinance a home loan in Australia?

Ans: The ideal time to refinance is when your fixed rate is ending, when market rates drop, or when your financial situation has improved. Many borrowers also refinance every 2–3 years to stay competitive and avoid reverting to higher “standard variable rates.”

Q2. Does refinancing always save money?

Ans: Not always. Refinancing can lower repayments and interest costs, but savings depend on break fees, exit fees, valuation results, and long-term loan structure. Comparing your current loan against multiple lenders ensures you avoid products that look cheap upfront but cost more over time.

Q3. Can I refinance if I want to consolidate credit card or personal loan debt?

Ans: Yes. Many borrowers refinance to roll high-interest debts into their mortgage at lower rates. This reduces monthly repayments, but it’s important to avoid reusing credit cards afterward and to structure the loan so consolidated debt is paid off quickly.

Q4. How does my credit score affect refinancing options?

Ans: A stronger credit score gives access to better rates and premium products. Borrowers with scores above 700 typically receive more competitive pricing, while those above 750–800 may qualify for some of the lowest rates available.

Q5. Can I use equity from refinancing to fund renovations or investments?

Ans: Yes. If your property has increased in value, refinancing allows you to access equity for renovations, investment property deposits, or business opportunities. It’s best to keep investment borrowings separate and ensure total repayments fit comfortably within your income.

Corry Cincotta - Mortgage Broker & Property Investor

Meet Corry Cincotta, owner of Digital Finance Solutions. A passionate property investor committed to helping Australians achieve their financial goals.

.png)