Buying your first home in Australia is equal parts thrilling and terrifying. Between property inspections, scraping together a deposit, and decoding mortgage jargon, it's easy to feel completely overwhelmed.

Here's the thing: you don't have to figure it all out alone. A mortgage broker acts as your financial translator and advocate, helping you save money, time, and a whole lot of stress. Let's break down how a good broker actually helps first home buyers save smartly, not just find any old loan.

Why First Home Buyers Struggle in the Mortgage Maze

If you've ever tried comparing home loans online, you know how quickly it gets confusing. Every bank advertises "the lowest rate," but the fine print is packed with fees, insurance costs, and clauses that can cost you thousands over the life of your loan.

Common mistakes first-timers make:

- Fixating on interest rates while ignoring the total loan cost

- Missing out on government schemes like the First Home Guarantee or stamp duty concessions

- Overborrowing without factoring in actual lifestyle expenses

- Only comparing the big four banks and ignoring better options

This is where mortgage brokers for first home buyers earn their keep. They see the full financial picture, not just the headline numbers.

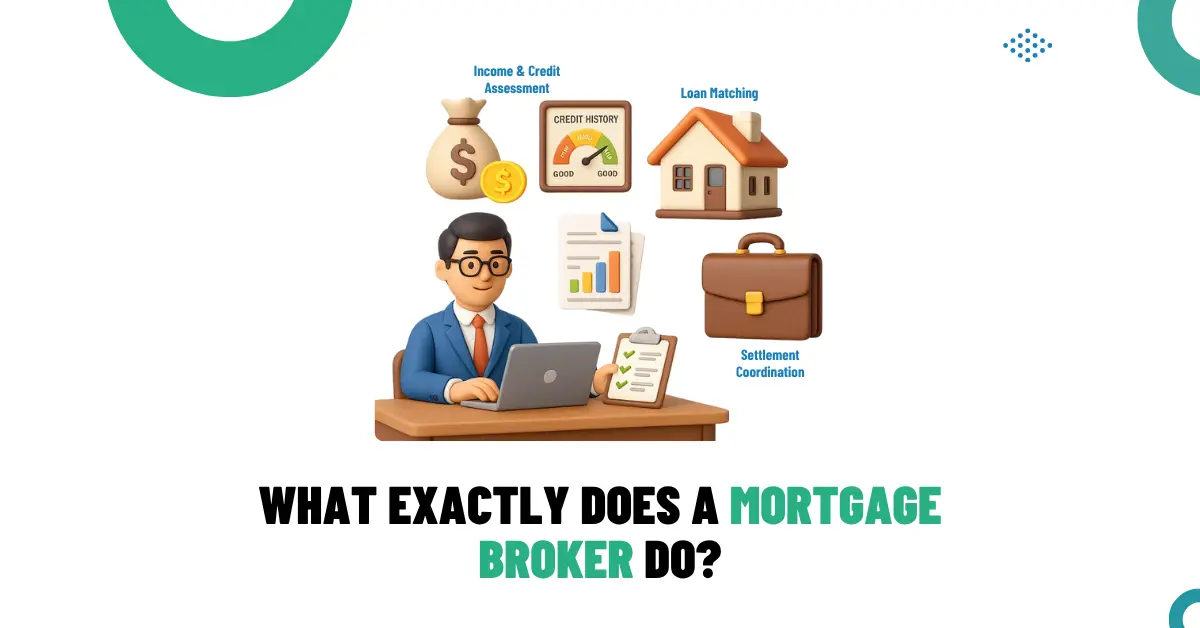

What Exactly Does a Mortgage Broker Do?

A broker sits between you and potential lenders: banks, credit unions, and specialist finance companies. Their job is to understand your financial situation and goals, then match you to the best loan across their entire panel of lenders.

Think of them as personal shoppers for home loans. Instead of you visiting ten banks, they compare dozens of products at once.

Here's what they actually handle:

- Assessing your income, savings, and credit history

- Matching you to loan products that suit your budget and deposit

- Preparing and submitting all the paperwork

- Negotiating rates and loan features on your behalf

- Coordinating with your solicitor, real estate agent, and lender right through to settlement

Unlike a bank employee, a broker isn't tied to one product line. That independence often translates into smarter options and real savings.

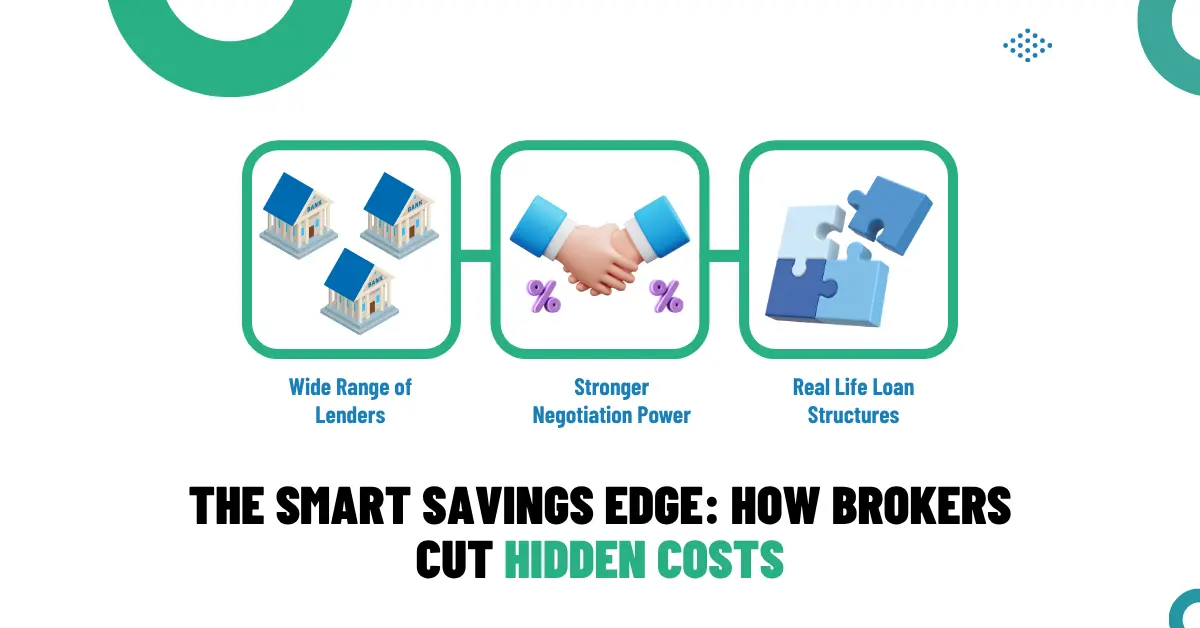

The Smart Savings Edge: How Brokers Cut Hidden Costs

Access to a Wider Range of Lenders

In Australia, some of the most competitive loans come from smaller lenders who don't spend big on advertising. Brokers often have direct relationships with these niche providers. More options mean more leverage, and that can easily shave tens of thousands off your interest bill across the life of the loan.

Better Negotiation Power

Brokers negotiate every single day. They know which lenders are flexible with credit history, which ones can waive annual fees, and which ones offer special rebates for first home buyers. Having that insider knowledge is like having a seasoned advocate at the table when the deal's being struck.

Loan Structures That Match Real Life

A low rate looks great until you realise the loan doesn't allow extra repayments or redraws. A smart broker helps you weigh features that align with your long-term goals: offset accounts, flexible repayment schedules, or variable/fixed splits. These structural tweaks quietly save you thousands.

Navigating Grants and Schemes You Might Miss

Australia's home ownership landscape is packed with opportunities that most buyers overlook. For example:

- First Home Guarantee (FHBG): Buy with as little as 5% deposit, no Lenders Mortgage Insurance (LMI)

- First Home Owner Grant (FHOG): Up to $10,000 for new builds

- Stamp Duty Concessions: State-specific, can reduce upfront costs by thousands

A broker doesn't just know these programmes exist. They help you qualify for them. They understand the subtle differences between state rules and make sure your application ticks every box so you don't leave money on the table.

Making the Process Less Stressful

Buying a home already demands enough emotional bandwidth. Adding loan paperwork, credit checks, and lender negotiations can burn anyone out.

Brokers simplify the entire journey by:

- Collecting and verifying documents once, not ten times

- Anticipating lender questions and smoothing out approvals

- Keeping communication clear so you always know what's next

That clarity and time saving alone are worth their weight in gold, especially for buyers juggling full-time work and weekend open houses.

Avoiding Rookie Financial Mistakes

Here's what often goes wrong when first home buyers try to DIY the mortgage process:

- Signing fixed-term contracts without flexibility to refinance later

- Ignoring comparison rates (which include most fees)

- Forgetting to budget for valuation, legal, and settlement costs

- Falling for "honeymoon rates" that spike after the first year

Refinance mortgage brokers know these traps inside and out. They guide you to sustainable choices that won't corner you when interest rates shift.

What to Look For in a Good Broker

Not all brokers are created equal. The right one feels like a partner, not a salesperson.

Ask these questions before committing:

- Are you licensed under ASIC and accredited with MFAA or FBAA?

- How many lenders do you work with?

- Do you specialise in first home buyers?

- How are you paid: commission, flat fee, or both?

- How often will you update me during the process?

Transparent answers build trust. You're entrusting this person with your biggest financial decision, so comfort and clarity matter more than charisma.

Step-by-Step: How to Work With a Broker

- Preparation: Gather payslips, savings records, and credit reports.

- Discovery: Explain your goals: first home, investment, lifestyle flexibility.

- Comparison: Your broker shortlists several loan options and explains the pros and cons.

- Application: They handle submission and follow-ups.

- Settlement: Your broker stays involved until the keys are in your hand.

- Post-purchase review: A good broker checks back after 12 months to see if refinancing could save you even more.

That ongoing support is what transforms a one-off transaction into a smart financial strategy.

Key Takeaways

- A mortgage broker's network opens more doors, literally and financially

- They decode complex loan options into clear, human language

- Smart loan structures and grants can save thousands in hidden costs

- Choosing an experienced broker means less stress and better results

In short, a skilled mortgage broker isn't an expense. They're an asset that helps first home buyers in Australia build wealth intelligently.

Final Thoughts

Buying your first home will always be a big milestone. But it doesn't have to be confusing or financially draining. A mortgage broker brings expertise, perspective, and negotiation power that most buyers simply don't have.

So before you sign a loan offer, ask yourself one question: "Do I have someone in my corner making sure this is the smartest choice for me?"

If the answer is no, it's time to talk to a trusted mortgage broker for first home buyers who can guide you toward confident, informed ownership.

Corry Cincotta - Mortgage Broker & Property Investor

Meet Corry Cincotta, owner of Digital Finance Solutions. A passionate property investor committed to helping Australians achieve their financial goals.

.png)